We have already heard that the two biggest wallet platforms of Nepal Khalti and IME Pay are going to merge soon. If this turns out to be true, it will definitely give a head-to-head competition to eSewa, which is currently leading the wallet market in Nepal. In this article, let us discuss how the combination of Khalti and IME Pay will benefit users and how (and if) this will be a threat to eSewa.

So, what’s in it for me and you? Imagine all my bill payments, money transfers, and online shopping combined in a single “IME Khalti” platform! No more hopping from this app to that for different payments. Khalti’s always been my go-to for paying my phone bill; meanwhile, IME Pay’s my hero for remittances. If they blend Khalti’s smooth tech with IME Pay’s remittance magic, we might get the best of both worlds. Nepal’s migrant workers would cheer, too.

Plus, with eSewa dominance the spotlight, this merger could light a fire under everyone’s butts. More competition means better goodies, lower fees, cooler features, and maybe even friendlier customer support. I think that this merger might cut their costs, and if they’re nice, they’ll pass the savings on to us.

So, what’s in it for me and you? Imagine all my bill payments, money transfers, and online shopping combined in a single “IME Khalti” platform! No more hopping from this app to that for different payments. Khalti’s always been my go-to for paying my phone bill; meanwhile, IME Pay’s my hero for remittances. If they blend Khalti’s smooth tech with IME Pay’s remittance magic, we might get the best of both worlds. Nepal’s migrant workers would cheer, too.

Plus, with eSewa dominance the spotlight, this merger could light a fire under everyone’s butts. More competition means better goodies, lower fees, cooler features, and maybe even friendlier customer support. I think that this merger might cut their costs, and if they’re nice, they’ll pass the savings on to us.

There are places where Khalti and IME Pay fail to match eSewa. Back in 2018, the company teamed up with Nepal Airlines for domestic and international rights in the app. On the other hand, Khalti’s stuck with just local flights.

Not just that, eSewa has the cross-border feature from 2024, which means Indian tourists can pay the merchant with PhonePe or Google Pay via eSewa’s QR codes. Khalti’s got something similar, but eSewa’s 425,000 merchants make it king here. IME Pay? Not even flexing that muscle.

Oh, and eSewa also has eSewa Pasal, which is like a mini online mall in the app where you can buy items easily. Khalti and IME Pay don’t have that yet. Plus, in village areas, eSewa’s SMS feature (no internet needed) has saved many when Wi-Fi’s a myth. And what’s even cooler is that I can even enter an ATM and pull cash from my eSewa balance (from NIC Asia).

There are places where Khalti and IME Pay fail to match eSewa. Back in 2018, the company teamed up with Nepal Airlines for domestic and international rights in the app. On the other hand, Khalti’s stuck with just local flights.

Not just that, eSewa has the cross-border feature from 2024, which means Indian tourists can pay the merchant with PhonePe or Google Pay via eSewa’s QR codes. Khalti’s got something similar, but eSewa’s 425,000 merchants make it king here. IME Pay? Not even flexing that muscle.

Oh, and eSewa also has eSewa Pasal, which is like a mini online mall in the app where you can buy items easily. Khalti and IME Pay don’t have that yet. Plus, in village areas, eSewa’s SMS feature (no internet needed) has saved many when Wi-Fi’s a myth. And what’s even cooler is that I can even enter an ATM and pull cash from my eSewa balance (from NIC Asia).

Remittances are another core spot. Even though eSewa has agents (112,000+), it's IME Pay that leads in the remittance part. While eSewa handles remittances via eSewa Money Transfer with a lot of agents, it’s not as laser-focused or trusted as IME Pay. Nepal’s huge remittance market (25% of GDP) craves specialized service, and IME Pay just feels right. Khalti’s user-friendly app could polish this strength. Post-merger, IME Khalti might dominate remittances, pulling users who prioritize sending money from abroad over eSewa’s broader.

Remittances are another core spot. Even though eSewa has agents (112,000+), it's IME Pay that leads in the remittance part. While eSewa handles remittances via eSewa Money Transfer with a lot of agents, it’s not as laser-focused or trusted as IME Pay. Nepal’s huge remittance market (25% of GDP) craves specialized service, and IME Pay just feels right. Khalti’s user-friendly app could polish this strength. Post-merger, IME Khalti might dominate remittances, pulling users who prioritize sending money from abroad over eSewa’s broader.

Khalti and IME Pay Merge

What is a Digital Wallet?

So, we’re diving into the world of Khalti, IME Pay, and their big merger buzz today. But before we get lost in the juicy details, let’s start with the basics of digital wallets in Nepal. A digital wallet is like your trusted friend, safely holding your payment information like credit cards, bank details, or other digital credentials. It’s fast, it’s easy, and, honestly, it’s a game-changer. Nepal’s wallet story started off with eSewa way back in 2009, and since then, it’s been a wild ride.Is it better than Mobile Banking?

Now, here’s the fun part of my own life. I’ve tried mobile banking. Yup, those apps my bank keeps pushing, but I keep running back to wallets like Khalti and eSewa. This is because Wallets pack the exact features I need, like paying my electricity bill, sending cash to my cousin, settling a loan, or even ticketing to concerts or shows, all in a few taps. Mobile banking, on the other hand, is like a grumpy uncle. It is slow, it is stingy with features, and I will have to spend 11. 3 extra while transacting between two different mobile banking apps. This is not the case with digital wallet transactions. Furthermore, Wallets charge lower fees, do not have annoying yearly renewal costs (banks love sneaking those in), and they just feel more… me. In Nepal, I’ve noticed (on Reddit, I mean) that most folks agree that wallets are a better option compared to mobile banking.Khalti and IME Pay teaming up

Okay, let’s talk about the hot gossip. Khalti and IME Pay might be tying the knot! As per the rumors, the companies signed a Memorandum of Understanding (MoU) on February 16, 2025, tentatively named “IME Khalti.” No official announcement has been made yet, but the news is flowing like monsoon winds. As someone who uses both apps, I’m kinda excited about this big news. Could this merger shake things up? Here's what I think.How this merger could benefit users

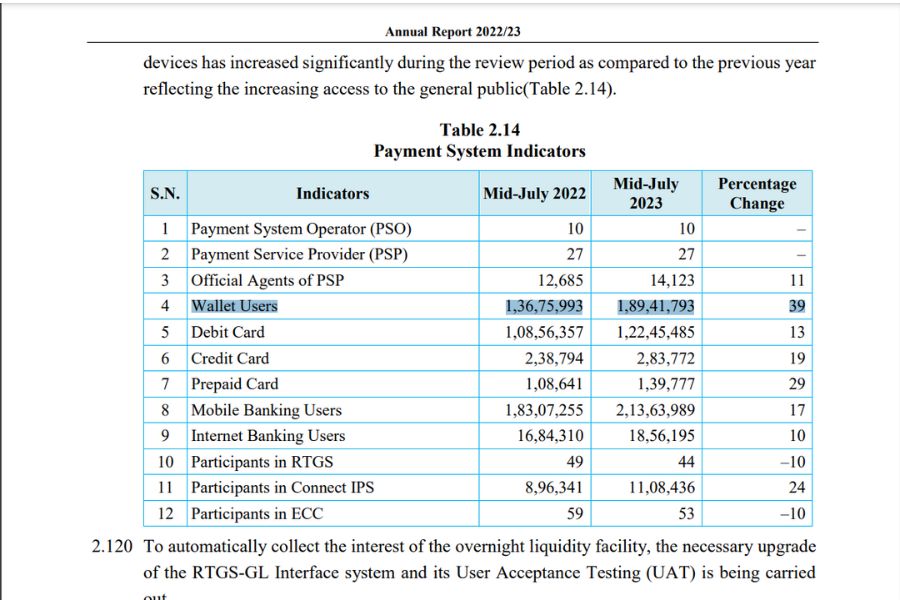

As per Nepal Rastra Bank, there are over 18.9 million wallet users (as of mid-2023), and Khalti claims around 5 million plus users and IME Pay with 5 million users. Add that up, and boom; IME Khalti could flex a 10-million-strong user base, staring down eSewa’s 8+ million (though their app’s hit 10 million downloads). For years, eSewa’s parent, F1Soft, has been the big boss of Nepal’s digital scene. Hopefully, this merger might bring this year’s long dominance down or at least bring some change.eSewa: The OG that’s still got swagger

But hey, everything I said earlier does not come that easily. Now, let’s chat about eSewa, the OG of Nepali wallets. Is this merger a threat to its crown? Honestly, I don’t think eSewa’s sweating bullets just yet. I’ve been an eSewa user since forever (it’s the first wallet I ever used), and it’s practically family for me now. After 15 years (born in 2009), it’s a name I trust, like my favorite chiya spot. With 80% of the market and 8+ million users, it’s got a fan base that’s tough to crack. Convincing someone to switch is a hard pass unless Khalti and IME Pay are coming with some insane games (offers) that people cannot just ignore.- Also, read:

eSwea is coming up stronger

Here’s the cherry on top: eSewa’s rumored to launch an IPO soon. Not because F1Soft’s broke (haha, they’re loaded!), but to let us regular folks buy shares. I’d love to own a piece of eSewa, I mean if I got lucky enough to get allocated (I have hard luck getting). That’s a loyalty hack I don’t think IME Khalti is planning on adapting anytime soon. Well, it’s not that perfect- picture as I just made it sound. eSewa’s app glitches sometimes (ugh, those lags!), but let’s hope they will fix this soon. There are some major features eSewa lacks.Khalti-IME Pay’s attack

As I already told you, eSewa’s not perfect, and I’ve felt the sting. The bank transfers usually cost NPR 5-10, and some merchant payments come with charges, too. This is because of the dominance thing. Likewise, Khalti gives you some cash back on top-ups or bills. IME Pay’s even sweeter with zero fees under NPR 10,000, plus 3% interest on the balance if you have got at least NPR 1,000 there. If both of these features got mixed, I might ditch eSewa for cheaper thrills.My Final two cents

So, here’s the thought from my side. eSewa’s is no doubt still the wallet king of Nepal, sitting pretty on its throne with years of trust and loaded money. But Khalti and IME Pay merging is like two underdog teaming up to tease the giant with a stick. With cheaper fees, remittance feasibility, and better feel, IME Khalti could make eSewa sweat buckets. But one thing is for sure: it won’t happen overnight. eSewa’s got numbers of loyal fans, and breaking that will take time. Let’s see how marketing will go. For that, we will have to wait for the official confirmation and app launch with new features.- Meanwhile, watch our OnePlus 13R review:

Article Last updated: March 9, 2025